Summary of the 5th edition of the webinar series «Les entretiens de l'ECODEF», on the theme of the evolution of our defence apparatus in the face of the threat of high-intensity conflicts.

The 5th edition of this webinar, entitled «How should our defence system evolve in the face of the threat of high-intensity conflicts?», was broadcast live on Tuesday 17 January 2023.

Moderated by the Engineer General of Armaments (2S) Olivier Martin, Chairman of the Chair's Steering Committee, this issue featured a discussion with Nicolas Baverez, Economist and historian, Doctor of History and agrégé in Social Sciences, Member of the Management Committee of Commentaire, and Julien Malizard, Doctor of Economics, Deputy Chairholder.

Why this theme?

Russia's war in Ukraine confirms the credibility of a high-intensity war in Europe. However, to prepare for this, the military will have to adapt, which will require budgetary resources to regain thickness and, more generally, move from a flow logic to a stock logic.

The purpose of this webinar was to present the economic and budgetary considerations the two guests : Nicolas Baverez with Bernard Cazeneuve, is the author of two Institut Montaigne reports on the transformation of defence policy since the end of the Cold War [1] [2] and Julien Malizard several recent contributions on defence budgets in France [3] [4].

The full webinar is available on the Chair's YouTube page.

Olivier Martin: Could you remind us of the main changes that have taken place since the end of the Cold War?

Nicolas Baverez : After the collapse of the USSR, peace was taken for granted and war impossible. Yet there have been many shocks: the attacks of 11 September 2001, followed by the «bogged down» wars in Afghanistan and Iraq. Despite this, the defence budgets of the Western powers have been on a downward trend (around -20 % in France in constant euros) between 1990 and 2015. France, for example, has maintained its nuclear deterrent and increased its force projection capabilities, but has considerably reduced the «depth» of its military capabilities.

In recent years, the strategic environment has been transformed by the rise of aggressive powers and authoritarian empires, as evidenced by Russia's invasion of Ukraine in 2022. Nevertheless, other threats, notably jihadist terrorism, still exist. In addition, new areas of conflict are emerging, such as cyber warfare, leading to hybrid wars. Finally, the hypothesis of high-intensity warfare has become more likely, which raises the question of adapting not only the military tool but also its doctrine of use.

Olivier Martin: How have the French armed forces adapted, particularly in terms of capabilities?

Nicolas Baverez : Until 2015, job cuts in the armed forces were intended to generate budgetary leeway to finance the modernisation and adaptation of the armed forces, as part of a «complete army model». However, these margins for manoeuvre were not created, and the trend in capabilities was therefore downwards until 2015.

From 2015 onwards, budgets have been on an upward trend, but they are not sufficient to meet the challenges of high-intensity warfare, because this requires a critical mass of stocks (ammunition or spare parts) and volume to last over time. For example, the number of shells fired per day by the belligerents in Ukraine is equivalent to the French army's stockpile. [5]. This has to be combined with the ramping up of a production base that was not designed for high-intensity use. For example, the last French order for CAESAR guns was placed in 2011, so exports have been essential to preserve industrial skills. The sample nature of the armed forces means that production capacity is limited. However, as the armed forces are part of a production system characterised by a cycle time that is much longer than that for civilian goods, adapting the industrial base requires considerable foresight.

Olivier Martin: Given the threat of high-intensity warfare, what budgetary resources should be allocated to the armed forces?

Nicolas Baverez : Before determining the means, we need to determine what we want to achieve in terms of strategic ambitions: to counter the existential threat of a major war, to protect the territory and the population, to contribute to the defence of the European continent within the framework of NATO. From this point of view, NATO has once again become a pillar of Europe's defence policy, although support for a European pillar of collective defence must continue. A closer partnership with Germany is therefore essential, despite the fact that relations have deteriorated significantly in political, military and industrial terms. In short, France will not face the high-intensity threat alone.

The ambition of being able to withstand high-intensity warfare requires us to fill certain major gaps (drones and munitions in particular). We also need to think about the volume of resources required to move towards a «war economy». Major changes in terms of defence effort are to be expected. For example, Germany plans to spend 2% of GDP on defence with a €100 billion modernisation fund, while the UK is aiming for 3% of GDP by 2030. In order for France to maintain its leadership at European level, a target of 3% of GDP seems credible. However, to reach it, we will have to look at the financing of other public spending, in a context of cannibalisation of the welfare state to the detriment of the sovereign state, rising interest rates and a level of public debt close to 120% of GDP.

Olivier Martin: What influence do budget constraints have on French defence spending?

Julien Malizard : Budgetary issues are at the intersection of economic and strategic questions. In an article published in 2022 with Josselin Droff, we quantified the role of each of these factors over the 5th Republic. The analysis shows that GDP is the fundamental determinant, while the level of threats, measured by the number of conflicts in the world, exerts a significant influence, albeit to a lesser degree.

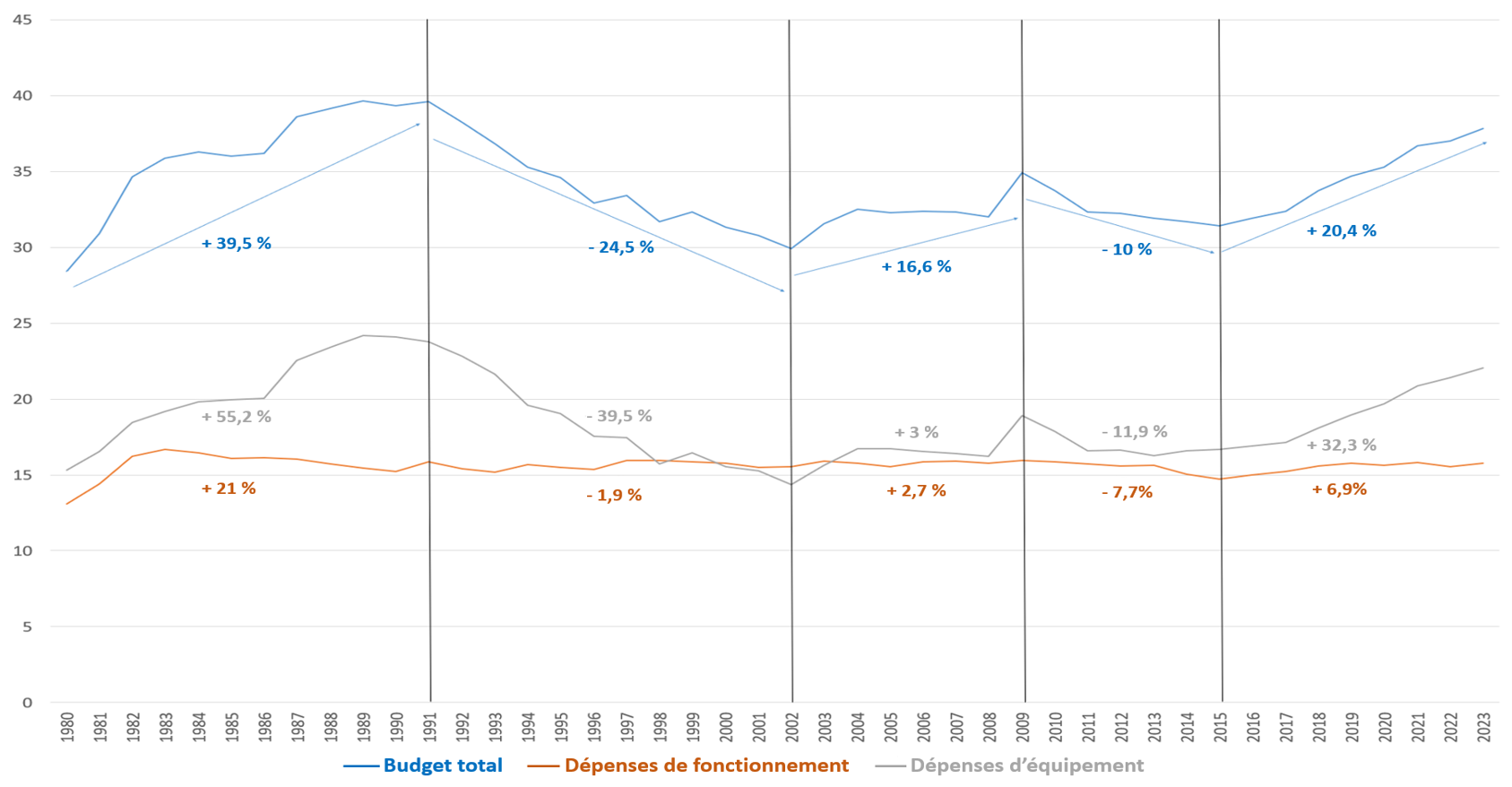

In addition, we can look at trends from 1980 to 2023 using data from the Ministry of the Armed Forces. The following graph shows the total budget (blue curve), capital expenditure (grey curve) and operating expenditure (orange curve).

The figures for 2022 and 2023 are based on inflation assumptions.

(Sources: Author's calculations, INSEE and Ministry of Defence data)

In the case of France, several periods can be distinguished in the evolution of the defence budget:

- During the Cold War, the budget increased structurally (almost 40% in real terms between 1980 and 1991). On average, strategic criteria dominated economic and budgetary issues.

- During the decade of the «peace dividend» (1991-2002), budgets fell after a wait-and-see period in 1991 (Gulf War). Economic conditions deteriorated significantly (1992 crisis) and the international situation no longer justified such a major effort in defence. The budget fell by 25% in real terms.

- With the attacks of 11 September 2001, budgets were on the rise until 2008 and the economic crisis that followed the collapse of the sub-prime mortgage market. This was also a period of relatively high economic activity and significant defence needs (Afghanistan, acquisition of modern platforms).

- Between 2009 and 2014, there was a relative decline, as a result of the «fiscal consolidation» policies implemented to consolidate public accounts. Budgetary constraints thus took precedence over strategic constraints.

- From 2015 onwards, following attacks on national territory, the strategic context changed for the worse (development of transnational terrorism in sub-Saharan Africa and the Levant, invasion of Crimea and Donbass). In conjunction with the action taken by the European Central Bank (ECB), this made it possible to free up margins for manoeuvre on public debt: defence budgets therefore started to rise again. Despite this increase, the level of the defence budget in 2023 will still be lower in real terms than in 1991 (around -4%).

In terms of composition, the defence budget is, on average (54 %), divided more in favour of capital expenditure, the other part being operating expenditure, essentially made up of the wage bill.

The trends in the two budget items are not identical. In fact, as Nicolas Baverez has just pointed out, operating expenditure has remained extremely stable over the overall period, despite a sharp reduction in staff numbers, whereas capital expenditure has followed a trajectory almost identical to that of total expenditure.

One reason for this is that defence equipment accounts for a large proportion of public investment, constituting a form of overall «kitty» that enables the State to cushion the ups and downs of the economic cycle. These factors confirm, at least for the period from the mid-1980s to 2015, that the Military Planning Acts (LPM) have not been implemented. This non-execution can be explained both by difficulties in anticipating the wage bill and by unrealistic budget assumptions which, in turn, constrain equipment spending. As a result, over this period, equipment orders were regularly revised downwards or postponed.

Olivier Martin: Where does France stand internationally, particularly in relation to our European partners?

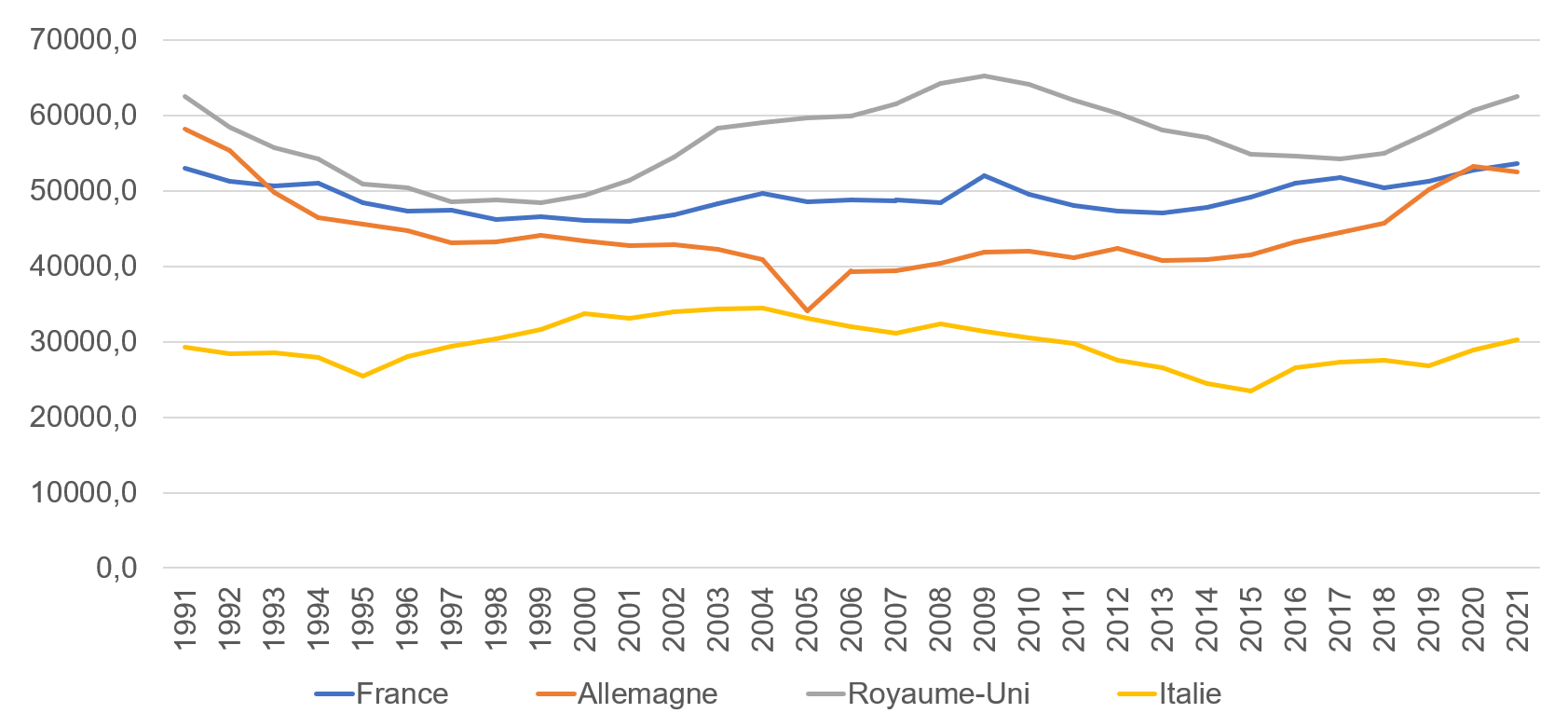

Julien Malizard From a long-term perspective, Figure 2 shows how France compares with its major European neighbours: Germany, Italy and the UK: Germany, Italy and the United Kingdom. The data used are those of SIPRI and are expressed in millions of constant dollars.

The cycles described in the previous section can be seen among European countries: according to SIPRI data, defence budgets in 1991 are close to those in 2021. Over the same period, US spending has increased by 30% [On the other hand, in a very different strategic context, China's defence spending has increased almost 12-fold].

The variation in French spending, both upwards and downwards, is smaller than that of its European neighbours. By way of illustration, the coefficient of variation (ratio between the standard deviation and the mean), which measures the dispersion of spending over a given period, is 4% for France, 12% for Germany, 9% for the United Kingdom and 10% for Italy.

For example, between 1991 and 2001, French spending was cut by 14%, compared with 30% in Germany and 25% in the UK (with a low point in 1999); between 2001 and 2009, the increase in the French budget was half (13%) that of the British (+27%). Finally, with the 2008 crisis, the «austerity cure» was much more severe in Italy (-22%) and the UK (-13%) than in France (-8%).

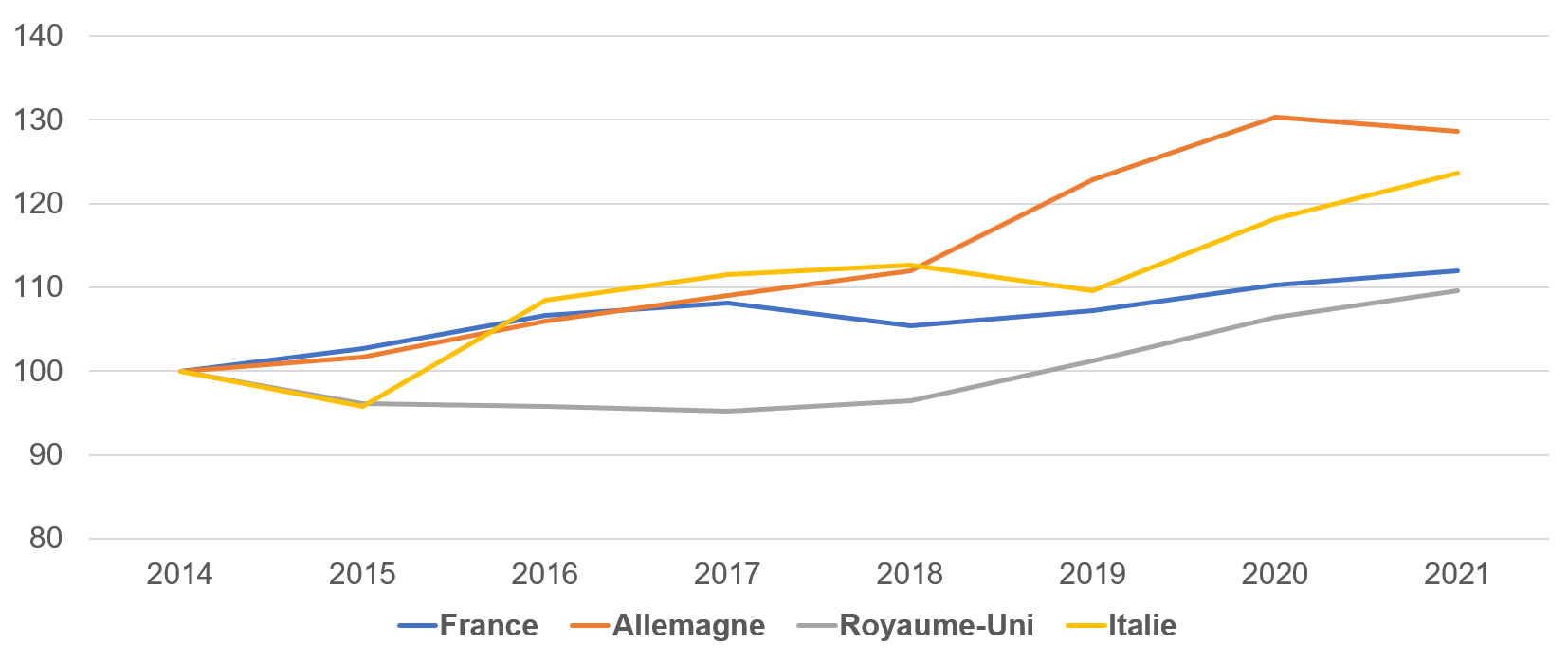

The invasion of Crimea was an electroshock for many European countries, which realised that the strategic environment on Europe's borders had been turned upside down. At the same time, the budgetary leeway regained by accommodating monetary policies has also enabled European states to finance this need for defence. The following graph presents a budgetary analysis centred on the period 2014-2021, expressed in base 100 using SIPRI data.

Over this period, French spending increased by 12%, compared with almost 30% for Germany and almost 25% for Italy (with the UK at 10%). Latvia and Lithuania have almost tripled their budgets, while Estonia has increased its budget by 50% (not shown).

Main questions from webinar participants :

Q1: Do you think French and European public opinion is ready to accept a major investment?

Nicolas Baverez : We have seen dramatic changes around these issues. A country like Germany was a pacifist country; with the war in Ukraine, the position of the leaders and the population has changed considerably. In France, opinion polls are also positive. Things are also changing at European level. The European Union was built around the law and the market. Today, there is a growing awareness of the importance of defence, with a number of initiatives (notably the creation of the European Defence Fund, to cite a recent initiative).

Julien Malizard : In the case of Germany, the population seems to be in favour of greater support than German politicians have decided. The population has evolved more quickly. In France, the French have a very good opinion of defence, but the question of the trade-off between different types of expenditure is not asked (analysis in terms of opportunity cost). Until now, the demand for social protection was such that French citizens were not prepared to make sacrifices in terms of social transfers in order to increase the defence effort, as Nicolas Baverez pointed out. For the record, out of €1,000 of public spending, €260 went on pensions and only €30 on defence (the same as spending on security and justice).

Q2: Are the people of Europe prepared to accept war?

Nicolas Baverez : What kind of war are we talking about? France and the United Kingdom are involved in external theatres and their opinions have already accepted losses on these operations, albeit in limited numbers. However, these losses are not on the same scale as in a high-intensity war. As we pointed out earlier, the most important change is for Germany, with a real and necessary change in German opinion. Nevertheless, we have not yet been directly confronted with high-intensity warfare.

Q3: How do you see the risk of recourse to high-intensity conflict evolving depending on the outcome of the conflict in Ukraine?

Nicolas Baverez : The strategic landscape will be very different if either Russia or Ukraine wins. If Russia wins, we can anticipate further military intervention on their part. If not, the Russian threat will be less intense. However, I don't think there will be a clear victory and peace, but a situation similar to that in Korea, with a ceasefire and latent conflict. So the Russian threat is likely to last.

Q4: LPMs are often not implemented. How do you explain this?

Julien Malizard : There are several reasons for this. Firstly, there is regular under-budgeting in terms of appropriations, in particular to obtain government approval for the launch of new programmes. In addition, the expected budgetary resources have not always been realised (sale of frequencies, exports not carried out, property disposals, etc.). Secondly, the principle adopted by the political authorities that cyclical economic shocks could be cushioned by changes in defence investment. Between 1990 and 2000, the defence budget lost almost 7 to 8 billion euros as a result of the economic downturn and the European criteria for budgetary rules (Maastricht Treaty). Finally, we were also in a period of peace dividends.

Q5: Can European autonomy be financed to meet future needs? How can we cover our needs without turning to the USA?

Nicolas Baverez : Europe is not autonomous today. If we want to buy equipment in the very short term, the European defence industry cannot meet the demand. So we have to turn to the USA. The reality is that Europe has no strategic autonomy and we have an industry that has been cut to the bone because we wanted to benefit from the peace dividend.

What can we do? Obviously, our security will continue to depend on the United States, but with two major limitations: firstly, the domestic situation in the United States, in particular the extreme polarisation of the population, and secondly the relationship with China, which is becoming the United States' strategic priority. Given these limitations and the presence of other threats on our continent (terrorism or the protection of our external borders), Europeans can and must be present in many areas of defence and security.

Julien Malizard : Political science researchers point to the lack of coordination and common vision at European level in terms of defence and security policy. From an economic point of view, the issue is the sustainability of the commitment made by the Member States. To put it plainly, will the equipment orders be long-term and sustainable, or will the Member States carry out this one-off upgrade and then return to the levels of investment seen in the years preceding the Ukrainian conflict? Depending on the answer to this question, orders will be placed with European or American industry.

Q6: How should the budgetary effort be divided between the three areas of land, sea and air? What about the budgetary effort needed overseas and in particular in the Pacific with the threats from China?

Nicolas Baverez : With this Land/Air/Sea trade-off, there is a risk of falling back into sterile quarrels between staffs. What's more, space and cyber must be added to these traditional areas. We clearly have work to do in all these areas. The most important thing is to define how to reconstitute an effective operational capability for high-intensity conflicts. We need to stop spreading ourselves too thinly and create a force capable of responding to high-intensity conflicts.

Overseas, particularly in the Indo-Pacific region, we have a large population and significant wealth creation. We cannot guarantee everything with our military capability, but we can send out strong messages with a significant presence, which presupposes a major effort in the maritime domain.

Julien Malizard : From a historical perspective, we can look at what happened during the Cold War, when the defence effort was around 2.8% to 3% of GDP. The current budget would therefore be almost doubled if we were at the same level, which would certainly enable us to increase operational capabilities and stocks.

Q7: Can the war economy have a positive or negative impact on exports?

Nicolas Baverez : France has embarked on a major de-industrialisation process (11% of GDP compared with 23% in Germany). Armaments remains one of our key sectors. French orders were so low that the survival of the defence industry depended on our exports. So we mustn't give up these exports, but the industry needs to move upmarket in order to meet more stable and larger domestic orders, while continuing to be able to meet export needs.

Q8: Do you think that, given budgetary constraints and the need to prepare for high intensity, we can keep the full army model?

Nicolas Baverez : The full army model costs between 2.5% and 3% of GDP, so the LPM must be at this level to make this objective credible. Talking about power without the means to achieve it shows our limitations, especially in the current international context.

Julien Malizard : From one generation to the next, equipment costs more and more. The new model will therefore cost more, and this will have to be taken into account in budgetary policy. At 2.8% to 3% of GDP, will all the objectives be met, bearing in mind that spending on deterrence has been ring-fenced?

")